Contents

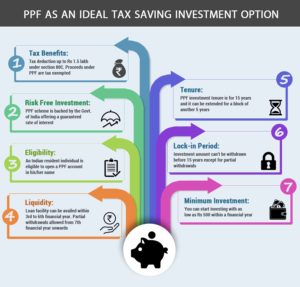

PPF or Public Provident Fund is a savings-cum-tax-saving instrument in India. It was introduced by the National Savings Institute of the Ministry of Finance in 1968. One can invest in it for the long-term to create a corpus for retirement. Its main features are its tax-free returns and the low risk attached to it. It is guaranteed by the Central Government of India. One can claim a tax deduction up to a maximum limit of Rs1.5 lacs for the amount invested in PPF under Sec 80 C.

Eligibility

Any individual who is a resident of India can open a PPF account. One can even open an account in the name of a minor of whom he is the guardian.

PPF minimum/maximum investment

As per the rules, one needs to invest a minimum of Rs.500 every financial year in his PPF account to keep it active. The maximum amount allowed for investment is Rs.1.5 lacs per year. If anyone invests more than that then the excess will not earn any interest and the authorities will return the excess to the investor. An individual can invest either as a lump sum or in monthly deposits. However, it is usually advisable to go for lump sum. The investment should be done before the 5th of April in order to earn interest for the whole financial year.

Duration

Initially, the authorities open the account for a period of 15 years. Post maturity, the individual can choose to extend it for another or multiple periods of 5 years each.

You may also like- ELSS or PPF: Which is a better tax saving investment option?

Procedure to open a PPF account

One can open an account online or visit any national bank, authorized private banks or post offices to open the account. It is useful to open the PPF account in a bank where one already has a savings account. So he can link both the accounts and during deposit, easily transfer the money from the savings to the PPF account.

Interest

The Ministry of Finance reviews and declares the rate of interest every quarter. The current rate of interest effective from 1 January 2018 is 7.6%. The Government calculates interest on the lowest balance between the fifth day and the last day of the month.

Maturity options

After the maturity period of 15 years is over, the below options are available to the investor:

- Complete withdrawal

- Extend the PPF account with no contribution:

This is the default option that is activated automatically if the person takes no action within the completion of 1 year of maturity. A person can withdraw any amount only once per financial year.

- Extend the PPF account with contribution:

The investor can choose to extend the maturity period by another block of 5 years. In this duration, he will have to continue investing in the usual fashion. With this option, a subscriber can only withdraw a maximum 60% of his PPF amount (amount which was there in the PPF account at the beginning of the extended period) within the entire 5 years block. An individual can withdraw only once in a financial year.

Conclusion

The Central Government guarantees the returns on PPF. So it is less volatile than equity investments. But if one wants to generate a higher corpus beating the inflation over the long-term then it is better to invest in equity through mutual funds and ELSS.