Contents

What is health insurance?

Health insurance is a type of insurance coverage that covers the cost of an insured individual’s medical and surgical expenses.

In health insurance terminology, a clinic, hospital, doctor, laboratory, healthcare practitioner, or pharmacy that treats an individual is known as the “provider.” The “insured” is the owner of the health insurance policy or the person with health insurance coverage.

Depending on the type of health insurance coverage, either the insured pays costs out of pocket and is then reimbursed, or the insurer makes payments directly to the provider.

In countries without universal healthcare coverage, such as India, health insurance is commonly included in employer benefit packages. It is often seen as an employment perk.

Why is it necessary?

We are at increased risk of falling prey to lifestyle diseases. According to estimates of various global and domestic organizations, with the increasing prevalence of lifestyle diseases in the country, one out of four Indians is at risk of dying from non-communicable diseases like cardiovascular ailments or cancer before the age of 70. Sticking to a healthy diet and following an exercise regime could keep many such unwanted ailments at bay. But, sometimes due to hereditary reasons and mostly with age, the chances of developing a life-threatening lifestyle disease increase.

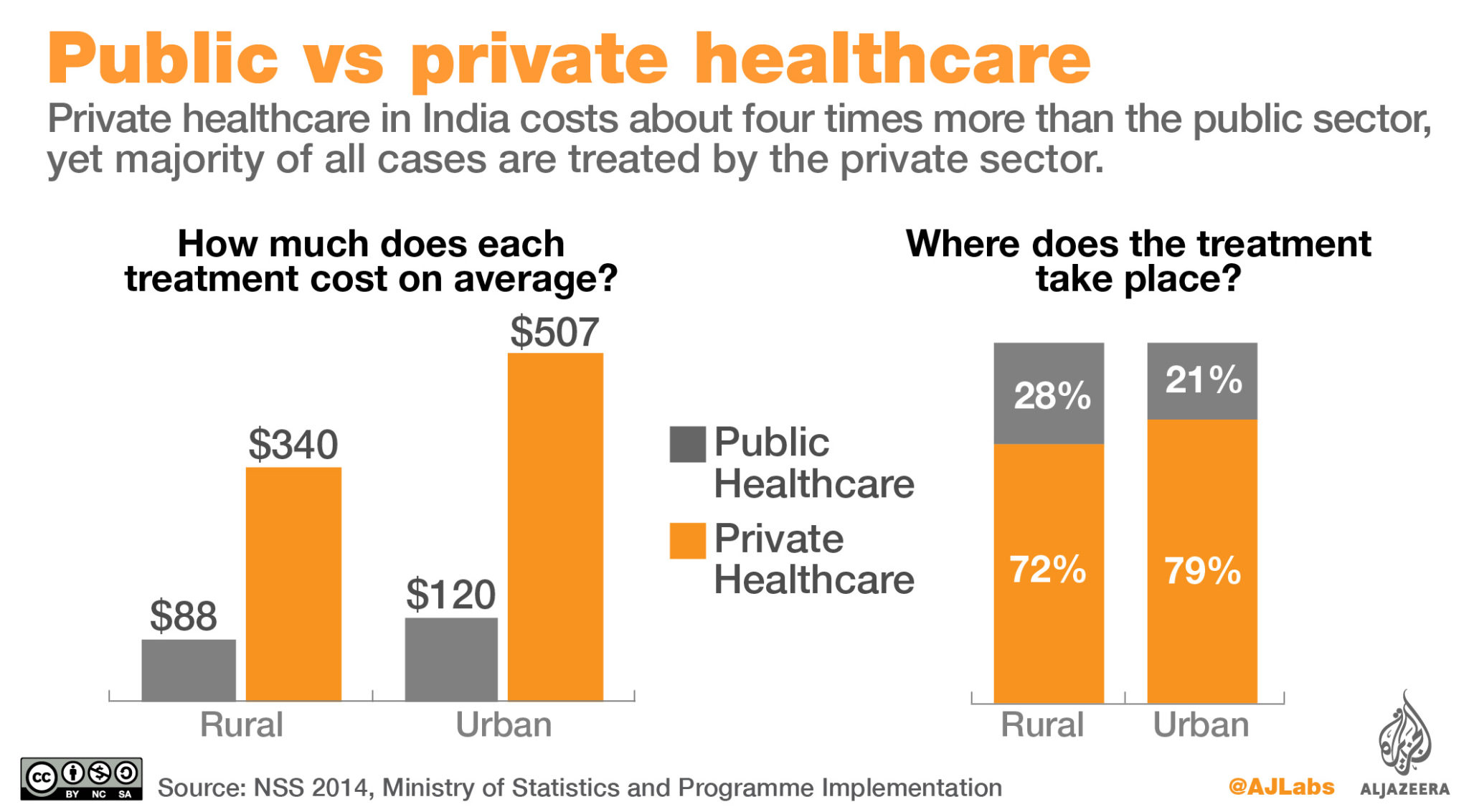

In today’s world, the cost of healthcare is rising at an alarming pace. The rate of healthcare inflation is close to 20% and is on the verge of increasing even more. If an individual gets diagnosed with a critical illness like Cancer, he will easily have to shell out lakhs of rupees for the treatment. That can burn a big hole in the pocket. Without a sufficient cover, he may need to dip into his savings and investments to cover the costs.

Types of health insurance

There are broadly three types of health insurance in India:

Hospitalization Plans:

Hospitalization plans reimburse the hospitalization and medical costs of the insured subject to the sum insured. For this reason, the plans are also known as indemnity plans.

The sum assured can be fixed –

i- For a member of the family in case of individual health policies or

ii- For a family as a whole in case of a family health insurance policy

For instance, consider a three-member family with an individual cover of Rs 1 lakh each. Each member can claim reimbursement for a maximum of Rs 1 lakh as all three policies are independent.

If the family applies for a family health plan cover of Rs 3 lakhs, then any family member can claim medical benefit for more than Rs 1 lakh so long as it is within the overall sum assured of Rs 3 lakhs.

Hospital Daily Cash Benefit Plans:

The daily cash benefit plan is a defined benefit policy. As evident from the name, the policy pays out a defined sum of money for every day of hospitalization regardless of actual costs. For instance, the hospitalization costs for a day may be Rs 2,000/day and the defined daily limit of the policy could be Rs 1,500/day, in which case the insured receives the latter. On the other hand, if the hospitalization cost is Rs 1,000/day, he still receives Rs 1,500/day.

Critical Illness Plans:

These are benefit-based health insurance plans which pay a lump sum amount on diagnosis of predefined critical illnesses and medical procedures. The illnesses are specified at the outset. By nature, critical illnesses are high severity and low frequency and cost of treatment are higher compared to regular medical problems like heart attack, stroke, among others.

Also Read: Term insurance plan 2018 | A must in India

Why is the employer’s health insurance not sufficient?

Most of us are offered Health Insurance as a prerequisite or benefit attached to our jobs. Because this insurance is built into our contract, we rarely analyze or compare it with other plans, never putting in the due diligence we would otherwise to buy other types of insurance. However, just because one does not have the option of rejecting an employer’s health insurance does not mean one should not analyze the pros and cons of these group plans. More often than not, these plans are limited in the cover they provide and come with problematic loopholes.

To demonstrate why and how employer’s health insurance plans may not be sufficient, we have outlined how these plans fall short, and how you can make up for their shortcomings:

Restricted Customization Options

Employers negotiate all aspects of the group cover—including the number of critical illnesses and diseases covered, inclusion of dependents, minimum and maximum sum assured— directly with the insurer, which means you cannot always ensure that the critical illnesses and surgeries you are prone to, given the familial history, are covered.

A fixed benefit plan offering various combinations of benefits and options for the sum insured, the inclusion of all family members along with the freedom to customize the payout for each benefit will help you take control of your family’s health.

Want cover solely for daily hospitalization expenses? A group plan is unlikely to offer such flexibility. This negative aspect can be overcome or nullified through a fixed benefits plan to cover hospital admission, specified surgeries, and numerous major critical illnesses for your entire family.

• No Guaranteed Continuation of the Plan

Employers offering group cover as a prerequisite or facility can always choose to discontinue the plan. Further, the coverage is linked to continuation in the job. Quit the job and the policy is automatically terminated. Unlike individual plans, a group plan cannot be extended or renewed for as long as one wants. The coverage will get terminated once the policyholder reaches the age of retirement. Moving from a group plan to an individual plan after retirement will always be costlier than renewing an existing individual plan.

An individual plan that can be renewed annually will be an expensive alternative offering no real benefits. What you need is a five-year fixed benefit individual plan that will ensure your family is protected irrespective of your employment status. From a family member needing ICU hospitalization for ten days to surgery for diabetes-related complications, the supplementary plan you choose must offer complete peace of mind.

- Little Scope for Planning for the Future The concept of group plans originated in an era when healthcare was not very costly and health insurance was not considered necessary. Hence, these plans focus on lowering the cost of the cover even if it involves the degradation of the quality of the care.

Will the plan reimburse the daily expenses resulting from hospital admission, even for a short period of just 7-10 days? Can you opt for surgery with absolutely zero worries about the cost of the procedure? Does the plan give you the confidence that no family member will lack proper care and treatment when suffering from a critical illness?

Group plans are suitable for routine and ordinary health expenses. To truly plan for the future, you need a plan that offers assured lump sum benefits at very lenient terms and conditions.

One needs a plan that effectively plugs the gaps in the group plan without unnecessary duplication of coverage. A fixed benefit plan like new HDFC Life Easy Health that gives you additional protection for recurring expenses during a hospital stay, surgeries, and treatment of critical illnesses combined with your group plan, will help you retain control over your family’s health cover well within the budget.

Group Plans Lag behind—the Numbers Story

Data obtained from a pan-India survey covering more than 3000 employees

• 59% of employees want coverage for general consultation as well. Only 39% enjoyed this benefit in their group plan.

• 31% sought inclusion of diagnostic services, which was offered by just 20% of employers.

• Only 28% of employers offered maternity education as a group plan benefit that was sought by 73% of all female employees.

Other Issues

• No option to customize plans to cover risks based on family history.

• Perfunctory coverage for surgeries and critical illnesses.

• High out of the pocket expenses during hospitalization.

How much is sufficient?

A health insurance floater policy of Rs 5 lakh is quite sufficient in most parts of the country. However, it may not be adequate if you live in a metro, where the cost of medical treatment is significantly higher. A 2-3 day hospitalization for common diseases can land you a bill of Rs 60,000-70,000 in private hospitals of metro cities. The bill for bigger ailments can run into several lakhs of rupees.

But a regular indemnity policy of Rs 3-5 lakh will not be of much use if the policyholder is diagnosed with a serious ailment. For such cases, a critical illness plan is more useful. But critical illness policies come at higher costs and cover only specific ailments. Still, they are better than some disease-specific covers.

Take a cover of at least Rs 7-10 lakh if you want to be on the safe side. Mercifully, the premium does not rise in the same proportion as the cover. If a Rs 5 lakh family floater cover is for Rs 12,000 a year, a Rs 10 lakh cover will not cost Rs 24,000. It will be for about Rs 18,000 a year.

The type of policy to buy should be determined by your family’s needs. The number of family members and their age is crucial to identifying a policy. For instance, a young family can do with a basic cover of Rs 5 lakh, while a family with older members should opt for a larger floater cover. Family floater premiums are linked to the age of the oldest member. If the parents are over 50, it would be sensible to get a separate cover for them, and not include them in the floater plan.

Tax benefits of health insurance

Premium paid towards health insurance for self, family and parents not only provides financial help in case of medical emergencies but also reduces tax liability. Here’s how.

Most financial planners suggest that the first step in any financial plan should be to ensure that one has adequate health insurance. One must get adequate health insurance cover for self and family even before starting to save for one’s goals. What’s more, the premium paid for health insurance also provides a tax benefit by reducing your taxable income and thereby your tax liability. Here are five crucial things to know about the tax benefits of health insurance plans as per income tax laws for fiscal 2015-2016.

Parents: The premium paid towards health insurance policies for your parents qualifies for deduction under Section 80D of the Income Tax Act. The benefit is available to individuals on health insurance premium paid for self, spouse, children and also parents. Importantly, it does not matter whether the children or parents are dependent on you or not.

The quantum of tax benefit, however, depends on the age of the individual who is medically insured. On the premium paid for self, spouse, children, and parents, the maximum deduction that can be availed is Rs 25,000 a year, provided the age of the individual is not above 60. If the premium paid by an individual is towards health policy for his or her parent who is a senior citizen of age 60 or more, the maximum is capped at Rs 30,000. A taxpayer may, therefore, maximize tax benefit under section 80D to a total of Rs 55,000 if his age is below 60 while parents age is above 60. For those tax payer individuals who are of age 60 or more and are also paying a health insurance premium for their parents, the maximum tax benefit under section 80D would, therefore, be a total of Rs 60,000.

Life insurance companies riders: The Section 80D tax benefit is on the premium paid towards health policy and therefore does not restrict one to buy health plan only from health insurance companies.

The premium paid towards critical illness or medical insurance riders in a life insurance policy also qualifies for tax benefit under the same section. Further, the premium on health insurance policies of life insurance companies is also eligible for the same tax advantage.

Health check-ups: Within the maximum limit of Rs 25,000 or Rs 30,000, the preventive health check-ups get a benefit of up to Rs 5,000. This means if you pay a premium of Rs 20,000 towards Mediclaim and undergo a health check-up costing Rs 5,000, the total of Rs 25,000 can be availed under section 80D. Most prominent hospitals offer preventive health checkup packages. With lifestyle ailments on the rise, it’s always better to keep an eye on one’s health.

Tax benefit available on both types of health insurance: Both ‘indemnity’ and ‘defined benefit’ kinds of health insurance plans would qualify for tax benefit. Not just the indemnity plans such as individual health insurance plan popularly called Mediclaim and Family Floater plans but also defined benefit plans such as daily hospital cash plan and critical illness plan of any standalone health insurance company or a general insurance company would qualify for tax benefit.

Cash payment: One may pay a premium in cash, however, in order to avail tax benefit, the income tax rules disallow tax benefit on premium paid in cash. One may, however, pay by Internet banking, cheque, draft or even by credit card to get tax advantage on premium. However, cash payment for preventive health checkup is eligible for section 80D benefit.

How to choose a health insurance plan?

With so many variants, this insurance product binds you to be particular while choosing the best health insurance policy in India. With the health insurance market flooded with thousands of plans, purchasing an adequate health plan is not a cakewalk! However, you may find the below pointers relevant while hunting for a health plan that meets your requisites.

Choose the Coverage Amount Smartly

Always go for the plan that offers maximum health coverage and maximum amount for the treatment. With medical inflation, health care expenses are going up drastically and therefore, you’ll need a sufficient amount to deal with the inflation. For instance, simple heart surgery costs around 4-5 lakh and for a middle-class family this amount is quite huge and it matters a lot if a medical policy covers this amount.

Family Floater Heal Plan is a Good Option

Individual health plans are designed keeping the needs of an individual in mind. However, if you are a family person, we will advise buying a family floater plan, which covers your entire family. This way you aren’t required to buy a separate policy for each member and can keep their health secured. The premium is also lesser as compared to individual plans and the sum assured is higher. Most importantly, anyone can utilize the amount during medical treatment. Also, you can cover your senior citizen parents as well by paying a slightly higher premium.

Choose the Sum Insured Precisely

Take the right sum insured based on your marital status and age. At a young age, the risk factor is less, however, your needs will evolve as you become older or cross 40. At this age, people may begin to be prone to a variety of illnesses including lifestyle diseases like diabetes, BP, etc. Similarly, once you are married, you should select the sum insured of your health plan considering the health status of your spouse as well.

Plan with Minimum Waiting Period for Pre-existing Illness

Every health insurance plan has its own set of terms and conditions regarding pre-existing diseases. It means if you have any disease prior to taking a plan, the claim made for taking treatment against that illness will be accepted after the insured serves a defined waiting period. In most cases the waiting period ranges anywhere from 2-4 years, however, some plans have a lesser waiting period like Mediclaim policy. While purchasing a health policy, you should opt for the one with less waiting period.

Maximum Age-renewal

You may not require a health policy at a young age but when you grow older, possibilities of health issues you encounter increases. So take up a plan, which you can renew at the age of 75 or 80 years of your age.

An insurer with high claim-settlement Ratio

Claim settlement ratio is the number of claims settled by the insurer over the total claims it receives. Always opt for a health plan from an insurer that has a high claim settlement ratio. This way you will ensure that your claim will not be rejected until the insurer has a valid excuse. However, you should be careful at the time filing a claim. Make sure you’ve attached all the relevant documents and proofs supporting your claim.

Go for the Plans with Sub-limits

Most of the health insurance policies come with sub-limits on per day medical expenses, room rent in case of hospitalization, etc. Consider those plans that offer the highest slab on room rent or other health care expenses. Well, the best health insurance policy in India always comes with the maximum sub-limits on health care expenses. You just need to select the plans, compare them online, calculate the premium and finally get the best deal for you.

Consider Network Hospital

With health insurance, you are entitled to avail treatments from network hospitals which are a group of hospitals associated with a particular insurer. For instance, if you are taking a health plan from Max Bupa, you can avail treatments from the hospitals that are in Max Bupa’s network hospital list. If you are purchasing a health plan for yourself/spouse or your parents or other family members residing in a rural area, always consider taking a plan, which has a wide network of hospitals in those areas. There is no point purchasing a plan if you are struggling to find an associated hospital to avail the cashless benefit.

Don’t Forget to Compare Premium

It is essential to compare the plans as well as the premium. There are many online aggregators that, help you compare the insurance policies in terms of benefits, features, premiums, maximum returns, etc.; picking a plan without weighing all the options available in the market is like inviting regret. By comparing the plans, you can avail all the benefits at a comparatively cheaper premium rate.

Don’t Ignore the Reviews

Reviews are essential when it comes to online purchasing. From grocery to medicines, clothes to footwear, electrical items and food orders, we are so inclined towards online services offered by various companies. The insurance sector is no exception. Many insurers have introduced insurance plans keeping the convenience of the customers in mind. And we often put a lot of stock by the reviews posted by other customers. In fact, reviews can make or break our decision to purchase any product or service. In the same way, what others’ experiences have been about the product certain health plan are very insightful. Reviews are always a mixture of negative and positive opinions which highlight the relevant pros and cons. This will help you take a firm and informed decision.

Mind the Exclusions

Most of the policyholders ignore this point and end up experiencing something unexpected. Exclusions are part and parcel of a policy and you can’t avoid it. If a plan covers something, it is equally entitled to not cover some illnesses, like some plans that exclude Hernia, Cataract, Sinusitis, Gastric, Joint Replacement, etc. in the initial period. While some others exclude expenses incurred on dental treatment, HIV/AIDS, eye-related healthcare, STD, cosmetic surgery, etc. You should choose a health plan with fewer exclusions.

Add-on Rider/Critical Illness Rider/Accidental Rider

With a critical illness rider, you ensure that your financial planning would not get disturbed if any unplanned medical expense arises. Critical illness cover is an add-on rider which you can opt for by paying an extra premium. In return, you can avail health coverage against those life-threatening diseases. We believe you won’t mind paying a higher premium if you’re getting a huge financial cover in return, right?

Things to Consider Before Buying a Health Plan

- Premiums

- No Claim Bonus

- The waiting period to be served for pre-existing ailments

- Co-payment

- Is there any waiting period for a specific illness?

- Incurred claim settlement ratio

- Maximum renewal age period

- Critical Illness add-on option

- Network hospital.

Well, this is not a comprehensive list however, we believe you will find this helpful in taking a firm decision at the time of purchasing a health plan.

With a plethora of health insurance policies, it is quite a tedious task to find the best health insurance policy in India. That’s why it is a wise decision to take help from comparison tools online. There are innumerable premium calculators or insurance calculators that help you find the best deal. This way you can bargain with the insurer regarding the premium. Also, at the time of renewal, you can compare what the other insurers are offering in the same plan. If you find them alluring than yours, switch your insurer. Also, do not forget to transfer your earned No Claim Bonus at the time that you change the insurer.